Eric Osiakwan

I conclued my last oped on the prognosis that exits would follow African scaleups and by that I meant some of the deals would be mergers, others would be acquisitions, whilst a third category may go public. The drafting and publication of this paper was delayed by the massive internet outage in West Africa, caused by the severance and disruption of four subsea cables. The incident drew my attention to the need for a resilient internet infrastructure in Africa, a subject on which I am currently writing a paper to compliment this interview I granted as part of a panel discussion on Africa’s internet resources. Without a resilient internet infrastructure, we risk a faulty foundation on which we build startups, scaleups, mergers, acquisiton and initial public offerings (IPOs).

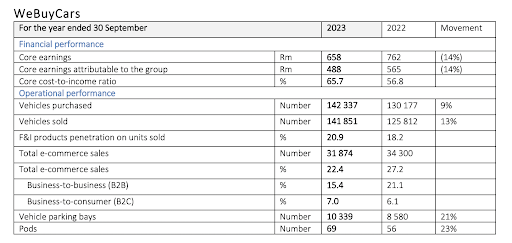

On the 8th of May 2024, Lesaka Technologies, a NASDAQ listed fintech with market capitalisation of $242M announced their acquisition of payment platform Adumo for $85K in a combination of cash and equity. On the 11th of April 2024, WeBuyCars, a South African online car +auction platform went public on the Johannesburg Stock Exchange (JSE) raising $444M instead of their anticipated $420M – signalling a return to both the international and local public markets for African tech ventures. At the end of April, BuuPass, a Kenyan travel booking platform acquired QuickBus with operations in Nigeria and South Africa. This followed Rivia – a Ghanaian healthtech service provider acquiring Waffle a SaaS sofware company to expand it’s offering to primary healthcare providers in early April.

in 2024, indicating that the leading Africa public market player is going to turbo charge IPOs across the continent – WeBuyCars was the first coming online at the beginning of the second quarter, signaling that there may be more in store for the year. The Cape Town Stock Exchange (CTSE), the second largest stock exchange in South Africa, focused on small and medium sized business with growth potential focused on the South African and larger Africa market – it is the only exchange that lists both equity and debt – this makes for more liquidity. Last year, Barloworld, ABSA, Shoprite and PPC completed their secondary listings on the A2X, a Cape Town-based which does secondary listings, The Victoria Falls Stock Exchange which is based in Victoria Falls, Zimbabwe also does secondary lists. These are generating liquidity that is getting them investor attention to the African market.

Nigeria’s leading payment company, Flutterwave has announced going public next year on the NASDAQ and so has Airtel Mobile Money without disclosing details. These would herald a return to the international public markets for African tech ventures which would bring back the much needed investor attention. This would create a counter current to the funding winter for the flow of investment into the risky venture capital asset class. The compounded imapct of African tech ventures going public on both the local and international markets would have a cascading effect that would drive more early stage investments in the angel investment market. The private equity market would eventually feel the ripples – making for liquidity all around.

Flutterwave has scaled into multiple African markets haven raised $509M and is valued at $3B from it’s last $250M raise from the likes of Avenir, Visa Ventures and Mastercard. It powers one million businesses across the continet and has processed over 400M transactions worth $25B for clients like Uber, Wise and Microsoft. Four other African scaleups that could go public, get merged or acquired are Onafriq from South Africa, Cellulant from Kenya, Hubtel from Ghana and Djamo from Ivory Coast – these are from the KINGS countries of Kenya, Ivory Coast, Nigeria, Ghana and South Africa and are all fintechs.

Flutterwave, Onafriq and Cellulant are head on in the same category of payment infrastructure with frontprints in multiple countries and they are followed by Hubtel and Djamo who are also in the same category but are considered embeded fintechs because their payment infrastructure is not obvious. They are both scaling up now with Djamo going into Senegal whiles Hubtel going into Kenya, Nigeria and Cameroon soon. These are just a sample of the leading African tech ventures that are scaling up to merge, get acquired or go public – setting the tone for what is yet to come.